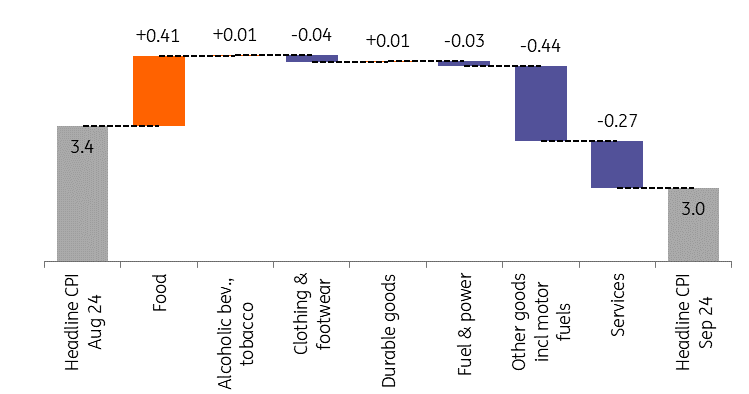

Inflation fell in September, hitting the central bank’s target for the first time since early 2021. Price pressures eased in services, but picked up in food. Despite the seemingly benign picture, it is FX stability rather than inflation data that will drive monetary policy decisions. Negative monthly repricing helps achieve inflation targetAs expected, inflation in Hungary eased further in September. The latest data came as a minimal downside surprise compared to market consensus, while in line with our expectations. Year-on-year inflation fell from 3.4% to 3.0%, reaching the central bank’s target for the first time since January 2021. That is a long 44-month journey, and while this is a welcome development, there is no time to relax as there will be some bumps in the road ahead.But before we talk about the future, let’s focus on the present. The further moderation in inflation was partly due to a 0.1% month-on-month fall in the average price level, and partly due to last year’s high base. So, at face value, we are happy campers. But if we dig deeper into the details, we find some interesting developments. Main drivers of the change in headline CPI (%)(Click on image to enlarge) Source: HCSO, ING The details

Source: HCSO, ING The details

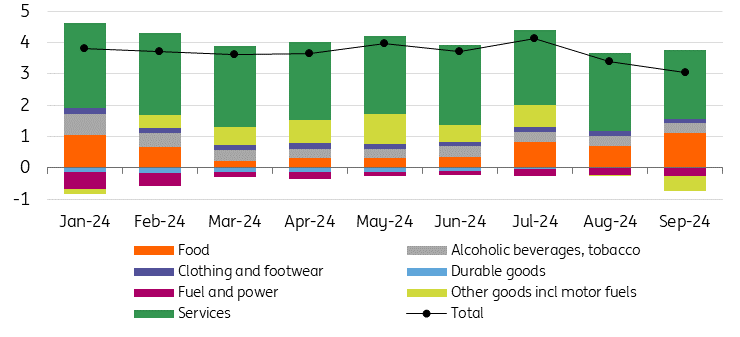

The composition of headline inflation (ppt)(Click on image to enlarge) Source: HCSO, ING Services keep underlying price pressure elevated, but big picture improvesAgainst this backdrop, core inflation remained much higher than the headline rate itself. And although prices here were flat on a monthly basis, the low base pushed the year-on-year indicator up to 4.8% in September. By contrast, the National Bank of Hungary’s measure of sticky price inflation moved lower by 0.4ppt to 5.4% YoY. The last time we saw a lower reading in this indicator was back in September 2021. Moreover, an important short-term indicator, the three-month annualised core inflation rate (3M/3M saar), has also declined.We can therefore conclude that several indicators signal that the underlying inflation picture is improving somewhat, although there is still work to be done from a monetary policy perspective. In particular, services account for almost three-quarters of the 3.0% inflation rate. This is important because this type of inflation is stickier than the price effect of items outside the core inflation basket. Headline and underlying inflation measures (% YoY)(Click on image to enlarge)

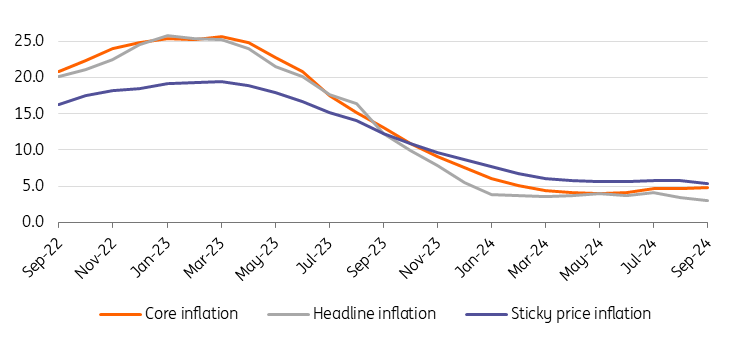

Source: HCSO, ING Services keep underlying price pressure elevated, but big picture improvesAgainst this backdrop, core inflation remained much higher than the headline rate itself. And although prices here were flat on a monthly basis, the low base pushed the year-on-year indicator up to 4.8% in September. By contrast, the National Bank of Hungary’s measure of sticky price inflation moved lower by 0.4ppt to 5.4% YoY. The last time we saw a lower reading in this indicator was back in September 2021. Moreover, an important short-term indicator, the three-month annualised core inflation rate (3M/3M saar), has also declined.We can therefore conclude that several indicators signal that the underlying inflation picture is improving somewhat, although there is still work to be done from a monetary policy perspective. In particular, services account for almost three-quarters of the 3.0% inflation rate. This is important because this type of inflation is stickier than the price effect of items outside the core inflation basket. Headline and underlying inflation measures (% YoY)(Click on image to enlarge) Source: HCSO, NBH, ING Inflation to accelerate temporarilyLooking ahead, inflation rates are expected to rise sharply next month, making the visit to the inflation target a short one. On the one hand, this acceleration is due to the low base, and on the other hand, monthly repricing is likely to be more powerful again. Fuel prices will push up inflation in the coming months as a result of oil price and exchange rate movements, and food prices may also continue to rise. Indeed, rising price pressures in these two items will also push up households’ perceived inflation, so that despite the positive statistical picture, households’ caution and fear of inflation are unlikely to ease towards the end of the year. According to our latest forecast, headline inflation could return to around 4.5-5.0% by December and core inflation to above 5%.Looking ahead to next year, inflationary risks are on the rise: the expected pick-up in consumption, continued dynamic wage growth (especially after a possible further significant increase in the minimum wage) and the government’s tax measures are likely to be passed on to consumers in the form of price increases over the course of 2025. We expect inflation to average 3.8% this year, rising to 4.0% on average in 2025.ECB Minutes Show What Difference A Few Weeks Can Make FX Daily: Fed Minutes Keep Dollar Supported Asia Morning Bites For Thursday, Oct 10

Source: HCSO, NBH, ING Inflation to accelerate temporarilyLooking ahead, inflation rates are expected to rise sharply next month, making the visit to the inflation target a short one. On the one hand, this acceleration is due to the low base, and on the other hand, monthly repricing is likely to be more powerful again. Fuel prices will push up inflation in the coming months as a result of oil price and exchange rate movements, and food prices may also continue to rise. Indeed, rising price pressures in these two items will also push up households’ perceived inflation, so that despite the positive statistical picture, households’ caution and fear of inflation are unlikely to ease towards the end of the year. According to our latest forecast, headline inflation could return to around 4.5-5.0% by December and core inflation to above 5%.Looking ahead to next year, inflationary risks are on the rise: the expected pick-up in consumption, continued dynamic wage growth (especially after a possible further significant increase in the minimum wage) and the government’s tax measures are likely to be passed on to consumers in the form of price increases over the course of 2025. We expect inflation to average 3.8% this year, rising to 4.0% on average in 2025.ECB Minutes Show What Difference A Few Weeks Can Make FX Daily: Fed Minutes Keep Dollar Supported Asia Morning Bites For Thursday, Oct 10