Image Source:

Image Source:

Asian markets declined, mirroring the moves in the U.S. overnight, as concerns about rising inflation led to a selloff in Treasuries and a negative sentiment towards China influenced market dynamics as trade tariffs from the incoming Trump administration remain a concern. MSCI’s regional equities index is set to post its largest single-day decline in over two weeks, erasing gains made on Tuesday. China’s main stock index has plunged to its lowest level since September, fuelled by ongoing investor anxiety about the potential for increased U.S. tariffs. The S&P 500 dropped by over 1% on Tuesday following a report that revealed inflation among U.S. service providers has reached its highest point since early 2023. Economic worries are dampening investor confidence across Asia, particularly in China, where there are growing fears of a potential deflationary spiral. This concern is compounded by credit yield premiums nearing their lowest levels since the global financial crisis, causing scepticism about investor appetite for a surge of deals in global debt markets. In China’s $11 trillion government bond market, investor sentiment has turned increasingly pessimistic, with 10-year bond rates recently hitting all-time lows, falling over 300 basis points below those of the U.S., even after the Chinese government, led by President Xi Jinping, announced several economic stimulus measures. In other markets, oil prices increased for the second consecutive day on Wednesday, driven by industry data showing another decline in U.S. inventories, while Bitcoin fell below $100,000.The dollar gained strength on Wednesday, supported by rising Treasury yields following robust U.S. data that reignited concerns about a potential rebound in inflation. This left European stocks facing a sluggish start as traders prepared for differing monetary policy trajectories. While traders are becoming accustomed to the prospect of a gradual interest rate reduction cycle from the U.S. Federal Reserve, they anticipate significant cuts from the European Central Bank, even after Tuesday’s data indicated that inflation in the euro zone accelerated in December. Markets are forecasting 99 basis points of easing from the ECB this year, while they expect the Fed to reduce borrowing costs by 37.5 basis points by the end of 2025, with the first cut fully anticipated in July. The benchmark 10-year Treasury yields reached an eight-month peak on Tuesday, as data suggested a resilient U.S. economy with a stable labour market but also indicated the re-emergence of inflation risks.Today’s calendar highlights include key economic indicators such as euro area confidence and producer price index (PPI) data. In the U.S., the ADP employment report will be released, along with the minutes from the Federal Reserve’s latest meeting. Additionally, a speech from Fed official Christopher Waller is expected, which may provide insights into the central bank’s views on current economic conditions and monetary policy.

Overnight Newswire Updates of Note

(Sourced from reliable financial news outlets)

FX Options Expiries For 10am New York Cut (1BLN+ represents larger expiries, more magnetic when trading within daily ATR)

CFTC Data As Of 3/1/25

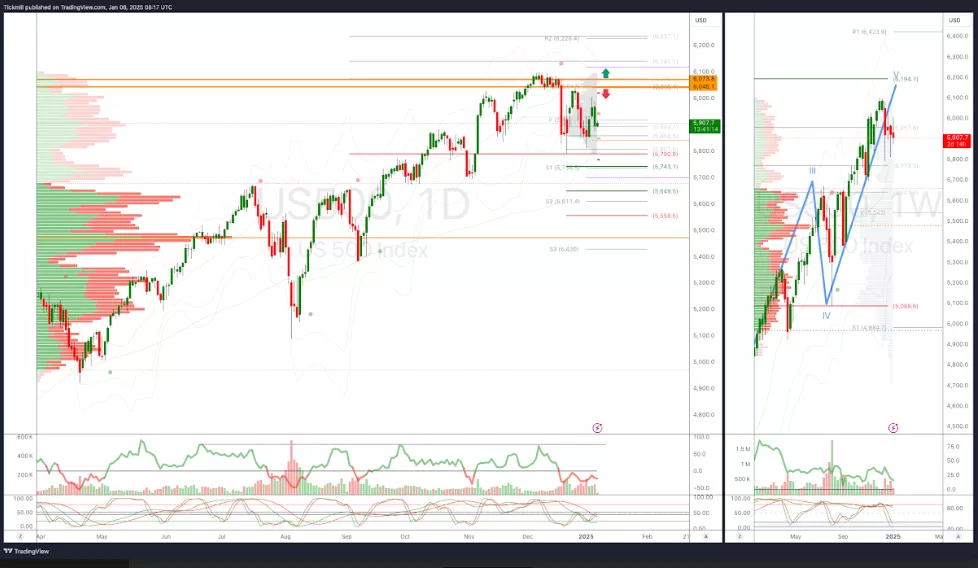

Technical & Trade ViewsSP500 Short Against 6045

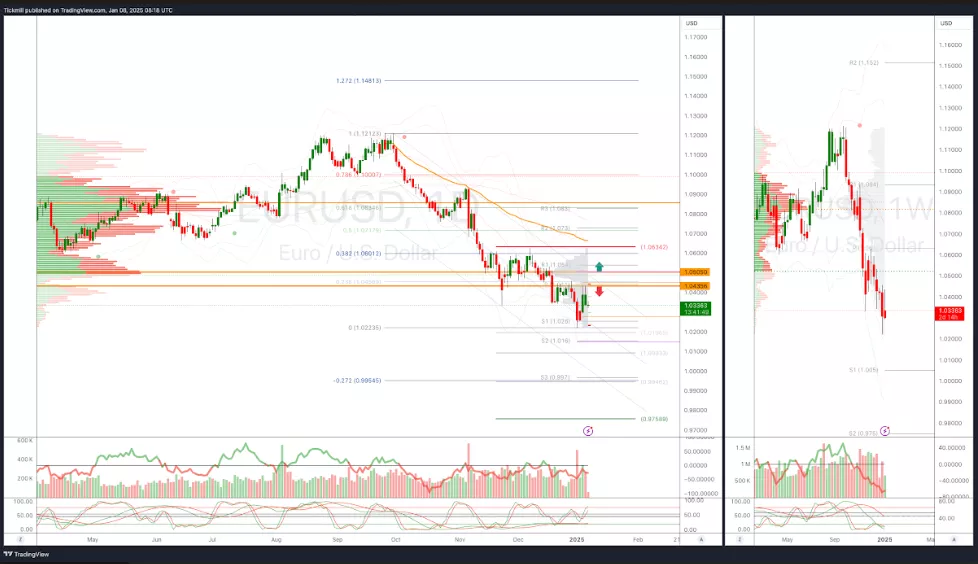

(Click on image to enlarge) EURUSD Short Against 1.0435

EURUSD Short Against 1.0435

(Click on image to enlarge) GBPUSD Short Against 1.2614

GBPUSD Short Against 1.2614

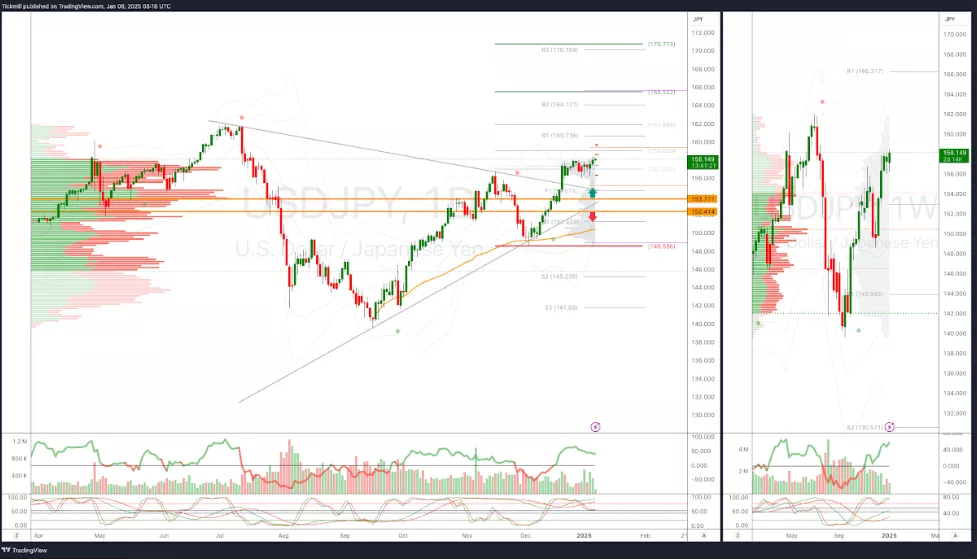

(Click on image to enlarge) USDJPY Long Against 153.77

USDJPY Long Against 153.77

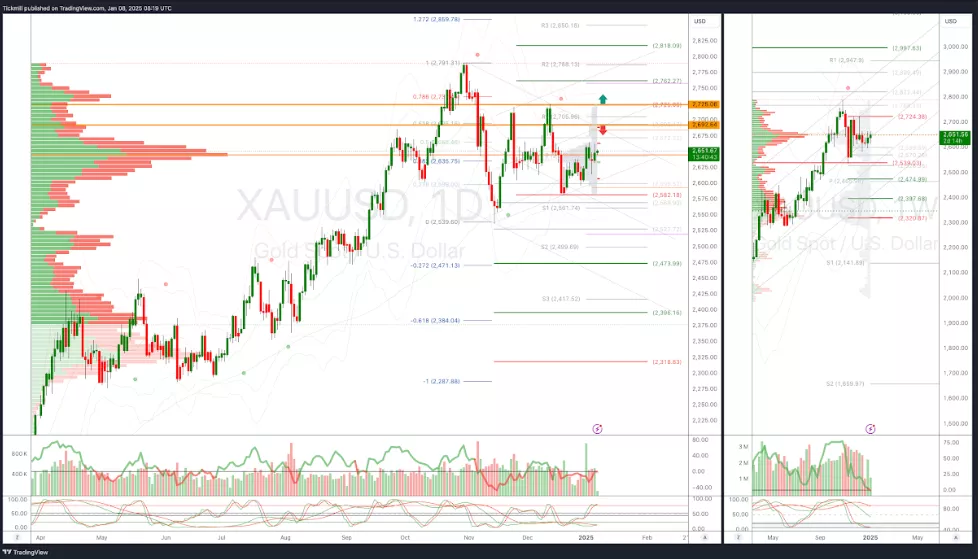

(Click on image to enlarge) XAUUSD Short Against 2692

XAUUSD Short Against 2692

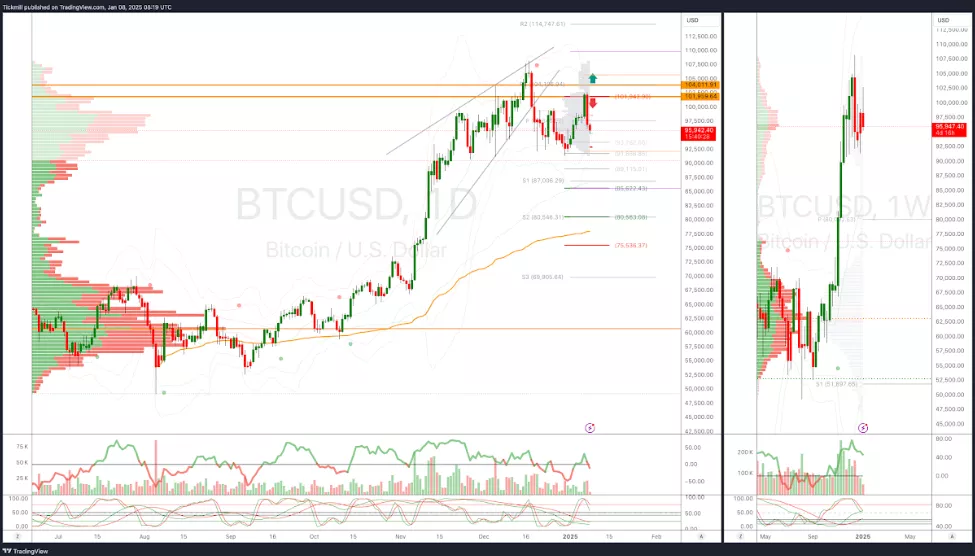

(Click on image to enlarge) BTCUSD Short Against 101,960

BTCUSD Short Against 101,960

(Click on image to enlarge)